Executive Summary

Contractors unbalance unit prices in their bids to take advantage of anticipated quantity overruns and underruns. An intelligent unbalancing of the unit prices can result in higher profits. Of course, that’s the contractors’ goal. Review the example provided to see how it’s done.

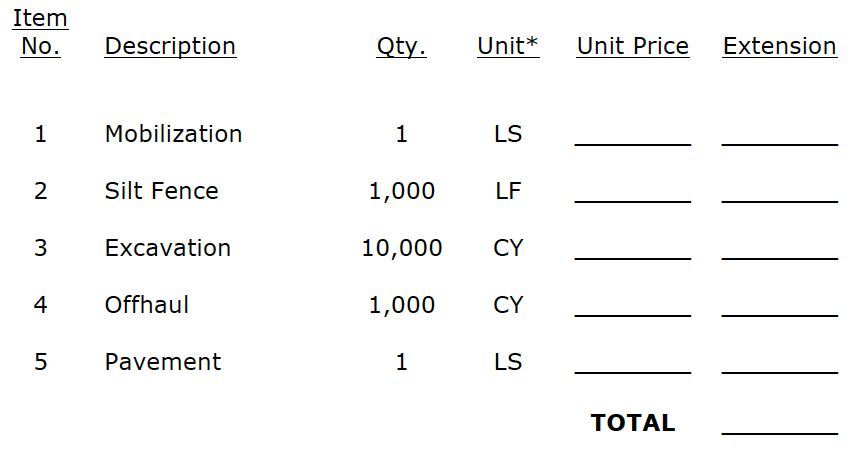

The Bid Proposal

Let’s look at a sample project which has had its bid proposal provided by the owner. The contractor must provide pricing on the bid proposal form provided by the owner with quantities provided by the owner. This is a typical unit priced bid.

This project has had its scope of work broken down into five bid items which are deemed adequate to encompass the entire scope of work for the project. Here’s our sample bid proposal:

*Units: LS = lump sum; LF = lineal feet; CY = cubic yard

Cost versus Revenue

You must understand this difference in order to grasp the concept of unbalancing. You also must grasp this concept in order to manage construction projects effectively. Here are the definitions:

- Cost – money spent by the contractor (money out the door)

- Revenue – money collected by the contractor (money in the door)

- Profit – the difference between cost and revenue (Profit = Revenue – Cost)

Schedule of Values is a Revenue Schedule and has Nothing to do with Cost

This concept is a tough one for many. I can’t tell you how many times a project engineer or a superintendent looked at the Schedule of Values with me and started talking about how much things were going to cost. The Schedule of Values (the bid proposal above become the mechanism of payment throughout the job and is often called the Schedule of Values) is simply a contractor’s schedule for revenue. It is not a budget. It is not cost. It is a means of getting cash in the door. It is a schedule of revenue designed by the contractor.

The Balanced Bid

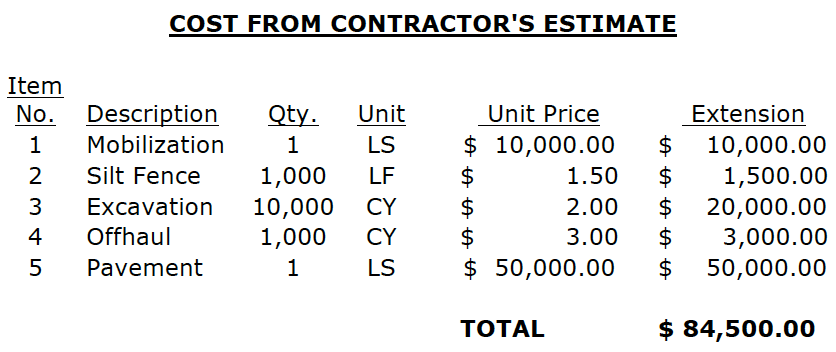

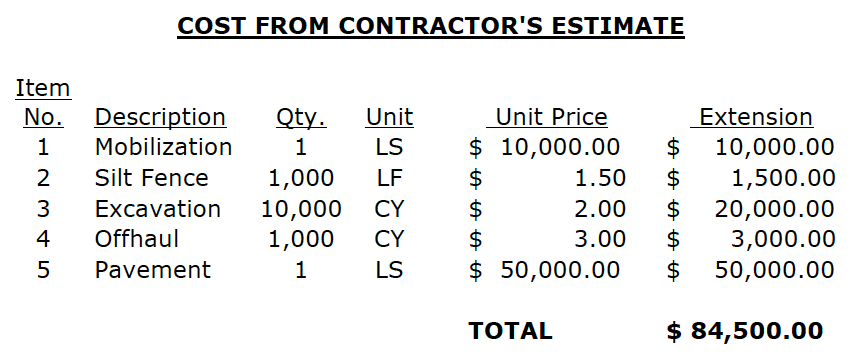

So, now that we understand what cost is and we understand that the purpose of a bid proposal (for a contractor) is to schedule revenue, let’s look at a balanced bid. Below is the cost of our bid – again, this is cost:

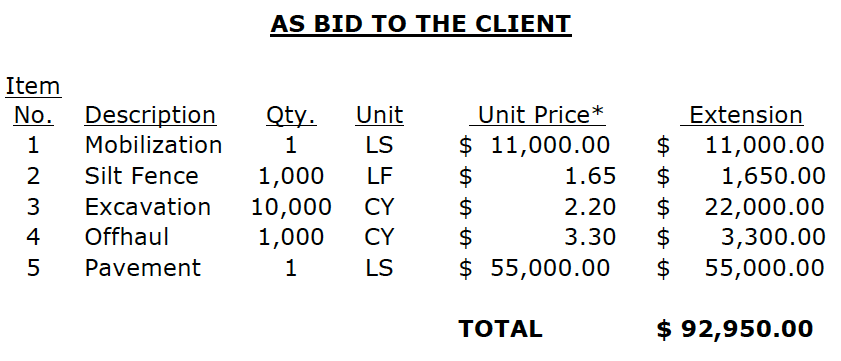

When we submit a balanced bid to a client, we evenly distribute our overhead and profit (OH&P) to each item in proportion to cost per item. So, our balanced bid (assuming a 10% OH&P) follows:

$, Profit $ 8,450.00

%, Profit** 10.00%

*Unit price is cost + 10.00% for OH&P (overhead and profit)

**Percent of cost (not revenue)

A balanced bid is when the overhead and profit are equally distributed to each bid item in proportion to their cost. Above, we evenly distributed the 10.00% overhead and profit (OH&P) in proportion to the cost of each item. This guarantees that we make 10.00% OH&P on the job regardless of quantities paid.

As you can see above we will collect $92,950 in revenue, we will spend $84,500, and this results in a profit of $8,450, or 10.00% profit:

Profit / Cost = 10.00%

$8,450 / $84,500 = 10.00%

And it follows, and is very important for this subject, that REGARDLESS OF QUANTITIES PAID the contractor still makes 10.00%. This is because each bid item is balanced and each item, regardless of quantity paid, pays the contractor his/her 10.00% OH&P.

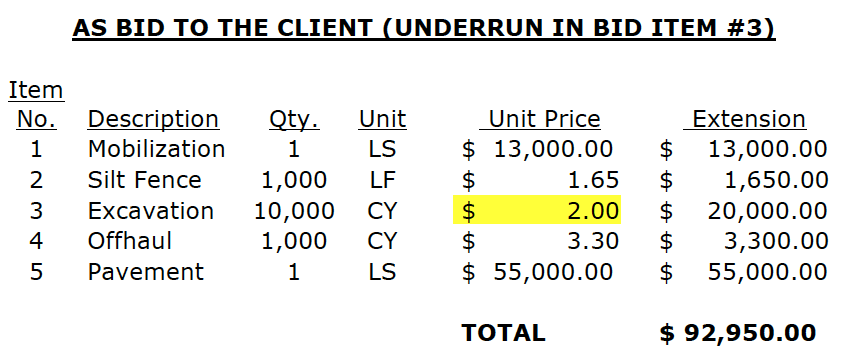

Unbalancing for an underrun in quantity.

If you’ve done a takeoff of the project and you know that the quantities in the bid proposal will differ from those performed and paid on the job, you may choose to unbalance the bid to increase profit.

So, as mentioned earlier, we still have to turn in a bid for the quantities on the client’s bid form even though we know they’re incorrect. So, our cost remains the same:

Below, we assume that the excavation quantity will underrun by 1,000 cubic yards. On bid day, we turn in the same bid amount of $92,950. But, notice that we have lowered our unit price for excavation from a balanced price of $2.20/CY to $2.00/CY (we have to also unbalance Bid Item #1 from $11,000 to $13,000 to maintain our bid amount). See the table below:

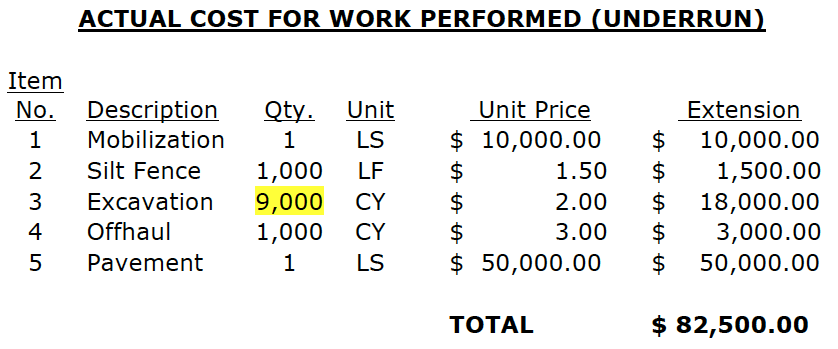

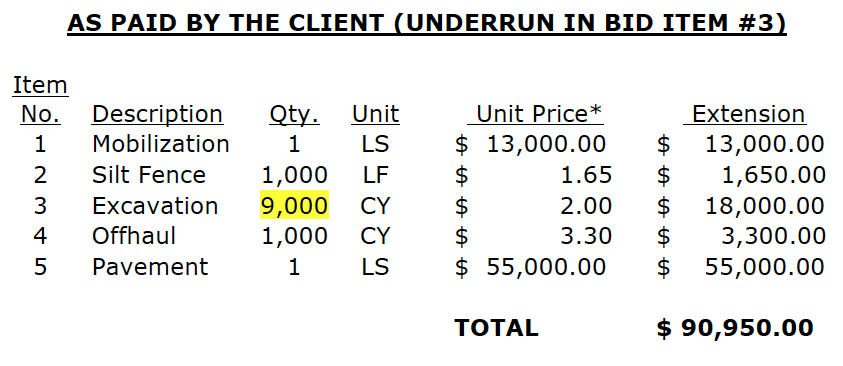

When the project has finished and we have only been paid for 9,000 CY (instead of the 10,000 CY in the bid proposal), we increase our profit margin from 10.00% to 10.24%. This is exemplified below by first showing the cost of our job based on quantities executed in the field (remember, we only performed 9,000 CY of the 10,000 CY in the bid):

From immediately above, we have incurred a cost of $82,500. Now, let’s see what the client paid us:

So, following from above:

Profit = Revenue – Cost

Profit = $90,950 – $82,500 = $8,450

Profit margin = Profit / Cost = $8,450 / $82,500 = 10.24%

The contractor’s margin has increased: 10.24% > 10.00%

Unbalancing for an Overrun in Quantity

The principle of unbalancing is the same in the case of an overrun. Now we have determined that the excavation quantity will overrun.

So, as mentioned earlier, we still have to turn in a bid for the quantities on the client’s bid form. Again, our cost remains the same for these quantities because we must assume for bidding sake that the quantities on the owner’s form are correct:

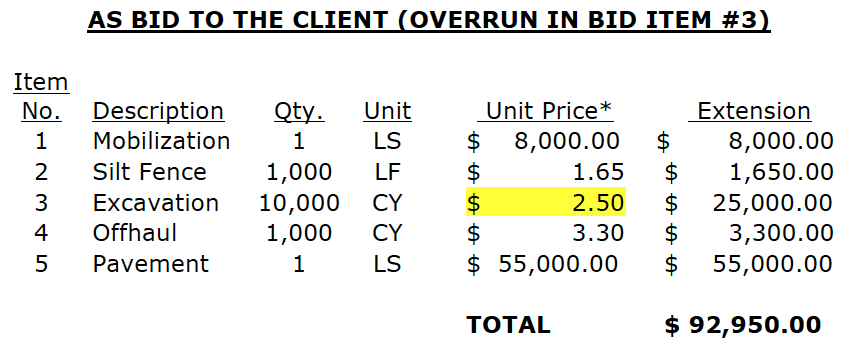

Below, we assume that the excavation quantity will overrun by 1,000 cubic yards. On bid day, we turn in the same bid amount of $92,950 as in both cases above. But, by unbalancing our bid by adjusting unit prices, we raise our unit price for excavation from a balanced price of $2.20/CY to $2.50/CY (we have to also unbalance Bid Item #1 from $11,000 to $8,000 to maintain our desired bid amount). See the table below:

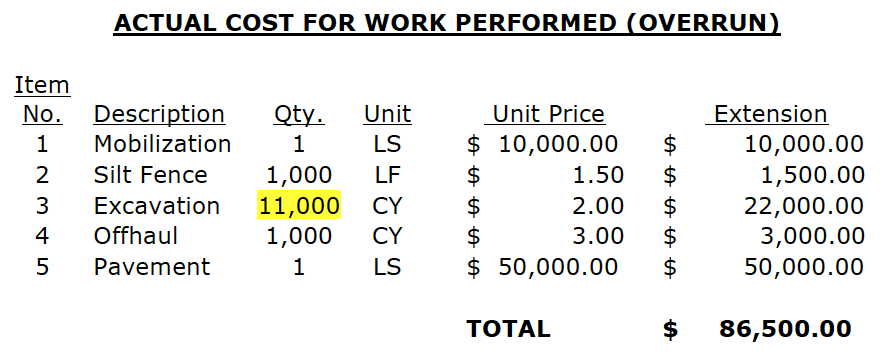

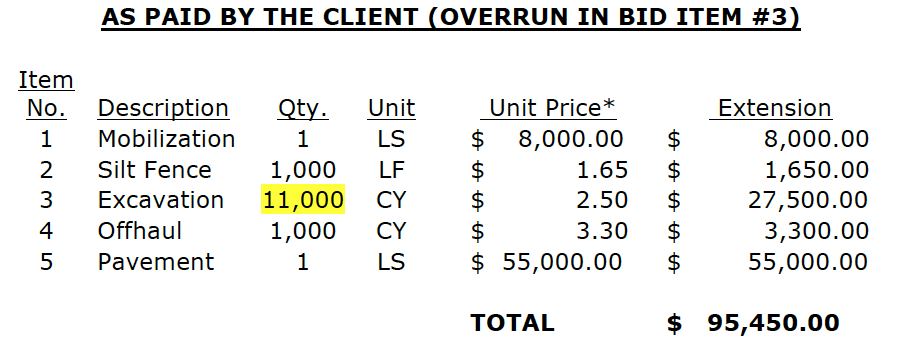

When the project has finished and we have been paid for 11,000 CY (instead of the 10,000 CY in the bid proposal), we increase our profit margin from 10.00% to 10.35%. This is exemplified below by first showing the cost of our job based on quantities executed in the field:

From immediately above, we have incurred a cost of $86,500. Now, let’s see what the client paid us:

So, following from above:

Profit = Revenue – Cost

Profit = $95,450 – $86,500 = $8,950

Profit margin = Profit / Cost = $8,950 / $86,500 = 10.35%

The contractor’s margin has increased: 10.35% > 10.00%

Notice that by turning in the same bid amount on bid day and adjusting bid unit prices to anticipate an overpayment of the excavation bid item quantity we increased profit margin from 10.00% to 10.35%.

Conclusion

The contractor was handed a set of plans and a bid proposal. This bid proposal usually turns into the Schedule of Values; the Schedule of Values establishes how each component of the work will be paid on a unit price basis.

Upon determining that the quantities in the bid proposal will differ from those paid [there will be an underrun or an overrun in a quantity(ies)], the contractor unbalances the unit price(s) to take advantage of this under or overpayment of the listed quantities. Based upon the quantities executed and paid, the contractor increases his/her profit margin.

Pitfalls and Advice in Unbalancing

The first thing to understand about this method is you better know what you’re doing before you implement it. You can read down below in the My Story section to see this work both ways.

Next piece of advice to you is to know the contract. Many contracts limit the percentage of allowable underrun/overrun in quantity and then make a unit price renegotiation available to owner and contractor.

Another thing is to be pretty sure that (a) your takeoff is correct and (b) that the inspector on the job will pay the underrun/overrun like you’ve assumed at bid time. Inspectors can be tricky and if there exists a precedent of horse trading instead of paying for underruns or overruns, you should figure that out ahead of time.

Lastly, make sure that your field supervisor knows which items are unbalanced – have an internal pre-construction meeting to handoff the estimate from the office to the field. A knowledgeable superintendent in this concept, and in the details of the particular bid, can play a huge role in increasing revenue (notice I didn’t say in decreasing cost!).

Rule of Thumb

The rule of thumb for unbalancing is that underruns are bid less than the balanced price and overruns are bid over the balanced price.

My Story

I unbalanced bid items in every unit price bid I ever turned in, sometimes for quantity differences, sometimes not.

When I did it for anticipated quantity variation, many times it didn’t make a significant difference because there was not that much swing in the quantities from the bid proposal to what was actually executed and paid in the field. A few times it did make a difference.

One example was on a $20 million highway job for a State Department of Transportation. Our estimators made a huge mistake; they didn’t do the unbalancing as described above and the quantity of dirt moved didn’t vary anywhere near the magnitude they anticipated. We lost about $5 million on that job and a major component of the loss was the unbalancing of the unit prices.

One job where it did go well was with a client that always removed paving from the job (they took the bid quantity of one lump sum and reduced it to zero). Look at my example above and assume the paving won’t be done. Say you bid it at a penny ($0.01/LS) which means that you took that $50,000 cost and put it in another item. If you were able to move all that money for paving into the mobilization or other bid items, that entire value of fifty thousand dollars became straight profit. I didn’t bid it at a penny, but I bid it at less than cost. That was a good job.

0 Comments